________________________________________

Key Updates on the Economy & Markets

________________________________________

The major development in 3Q24 was the Federal Reserve’s decision to cut interest rates by -0.50%, the first rate cut of this cycle. It came as the Fed shifted its focus, with unemployment rising to a 33-month high and inflation moving back to target. In the equity market, stocks ended the quarter higher despite some turbulence, including a brief but sharp sell-off in early August. The S&P 500 posted its fourth consecutive quarterly gain and ended September near an all-time high. This letter recaps 3Q24, discusses the Fed’s first rate cut, examines the increase in market volatility, and looks ahead to the final quarter of 2024.

________________________________________

The Federal Reserve Cuts Interest Rates by -0.50%

In 3Q24, the Fed started the process of normalizing interest rates after a volatile five years. To recap, the Fed cut interest rates to near-zero during the COVID pandemic to support the economy. It kept rates near 0% until March 2022, when it began raising interest rates in response to soaring inflation. From March 2022 to July 2023, the central bank raised rates by +5%, one of the largest and fastest rate-hiking cycles in recent decades. The Fed held interest rates steady for over a year as it waited for inflation to return to its 2% target, and after 14 months, it started the rate-cutting cycle with a -0.50% cut at its September meeting.

The Fed’s transition to cutting interest rates comes as its focus shifts from lowering inflation to supporting the labor market. Since the last rate hike in July 2023, inflation has dropped from 3.3% to 2.6%. However, over the same period, unemployment has risen from 3.5% to 4.2%, the highest level since October 2021. The Fed is more confident that inflation will return to its 2% target, but it’s concerned about the health of the U.S. labor market. The key question for the Fed and investors is what the labor market softening over the past year represents. Is the labor market simply normalizing after experiencing significant disruption during the pandemic, or is it an early sign of weakening labor demand? This uncertainty is one reason the Fed moved to cut interest rates.

Investors expect the Fed to cut interest rates at its two remaining meetings this year, with further reductions expected throughout 2025. The market expects an additional -0.50% of rate cuts by the end of this year, followed by another -1.50% by the end of 2025. Investors are betting that the combination of falling inflation and rising unemployment will cause the Fed to implement significant rate cuts. History indicates the actual timing and amount of rate cuts will depend on the economy’s path. A weaker economy would justify more rate cuts, while a stronger economy could require fewer rate cuts.

_______________________________________________

Financial Markets Experience Increased Volatility

In early August, the stock and bond markets experienced significant volatility. Signs of investor angst started to appear during earnings season in July, when investors raised concerns about the high costs of developing artificial intelligence (AI) and whether future revenues would justify the expensive investments. A few weeks later, investors were spooked as unemployment rose from 4.1% to 4.3%. Investors worried the Fed had waited too long to cut rates and risked tipping the U.S. economy into a recession that could be hard to reverse.

This sudden surge in market volatility caused investors to sell stocks and buy bonds, leading to a significant deleveraging event across global financial markets. The S&P 500 traded down nearly -8% from mid-July through the first week of August. However, the volatility was short-lived, and the S&P 500 rebounded to end August with a modest gain. There was some residual volatility in early September as investors returned from summer break, but the S&P 500 again recovered quickly and set a new all-time high later in the month. The rise in market volatility marks a significant shift from the past 12 months of steady S&P 500 gains, but so far, investors have brushed it aside.

_______________________________________________________

Equity Market Recap – Stocks Trade Higher as Investors Rotate Within the Market

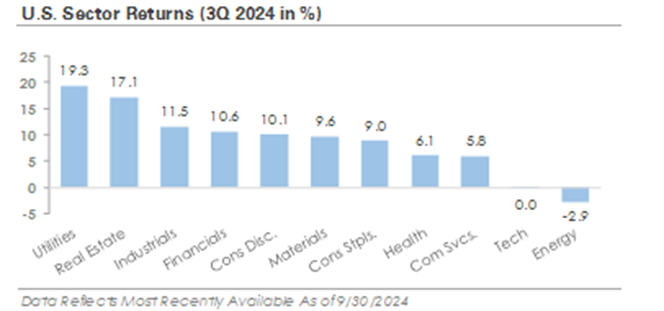

Despite the volatility, the S&P 500 set multiple new all-time highs in 3Q24, adding to its list of new highs from earlier in the year. However, it was the change in stock market leadership that made headlines. The Equal-Weighted S&P 500, the Russell 2000, and the Value factor all outperformed the S&P 500, while the Growth factor underperformed. A similar pattern occurred at the sector level, with underperformers from the first half of 2024 outperforming in 3Q24. Interest-rate-sensitive sectors outperformed in anticipation of rate cuts, with the Utility and Real Estate sectors both gaining over +17%. Cyclical sectors, including Industrials, Financials, Consumer Discretionary, and Materials, also outperformed the S&P 500. In contrast, the Technology sector lagged the market rally, ending the quarter flat after outperforming in the first half of the year.

Two key events, the Fed’s first interest rate cut in September and growing concerns about AI’s profitability, led to the change in market leadership in 3Q24. In the first half of 2024, uncertainty around Fed policy and concerns about the economy pushed investors toward large-caps and AI stocks. Meanwhile, smaller companies underperformed due to worries about their sensitivity to higher interest rates. With the Fed now officially cutting interest rates and doubts emerging about AI’s monetization potential, investors sought out new investment opportunities in 3Q24.

_______________________________________________

Credit Market Recap – Bonds Trade Higher in Anticipation of Interest Rate Cuts

In 3Q24, bonds traded higher as investors prepared for the start of the Fed’s rate-cutting cycle. The 10-year Treasury yield fell from 4.37% at the end of June to 3.79% at the end of September. The 2-year yield, which is a proxy for investors’ rate cut expectations, fell from 4.72% to 3.64% over the same period. Falling Treasury yields provided a boost to bonds overall, but there was an interesting dynamic within the credit market. The top two performing corporate bond groups were on opposite ends of the rating spectrum, but their returns were both linked to the start of rate cuts.

On one end, CCC-rated bonds, the lowest-rated and most sensitive to economic conditions, produced a total return of over +11% as corporate credit spreads tightened. The group’s outperformance suggests that investors expect interest rate cuts to stimulate economic growth and make refinancing easier. On the other end, AAA-rated bonds, the highest quality and most sensitive to interest rate changes, gained over +6% as the market priced in the first rate cut and yields fell. Together, the two groups’ outperformance indicates that investors expect rate cuts to boost economic growth and relieve pressure on highly leveraged companies.

_______________________________________________

Fourth Quarter Outlook – Themes to Watch

With the Fed beginning to lower interest rates, investors are focused on what happens next. The two key questions are how much the Fed will cut interest rates and how the economy will respond to those rate cuts. The next six months will be critical in providing answers to these questions, and investors will analyze each economic data point for clues about the economy’s trajectory. This intense focus on economic data may have the unintended consequence of keeping market volatility elevated as investors flip between optimism and pessimism.

As we wrap up this quarter’s market update, we want to briefly touch on the upcoming presidential election. With the election quickly approaching, you may be wondering how the outcome will affect financial markets and whether you should change your investment strategy. Political views can stir strong emotions but making investment choices based on those feelings can lead to poor portfolio decisions. Data suggests that whichever party occupies the White House has little to no impact on investment performance, with fundamental factors like corporate earnings growth and valuations impacting the stock market far more than political headlines. The U.S. economy’s success, growth, and resiliency don’t change with each new election, and neither should your long-term investment strategy.

![]()

________________________________________

Our mailing address is:

2827 Peachtree Rd NE, Suite #510

Atlanta, GA 30305

(404) 905-2290